Financial Coordination

The Coordination Gap: Why Affluent Households Lose Money Even When They Have a CPA and a Financial Advisor

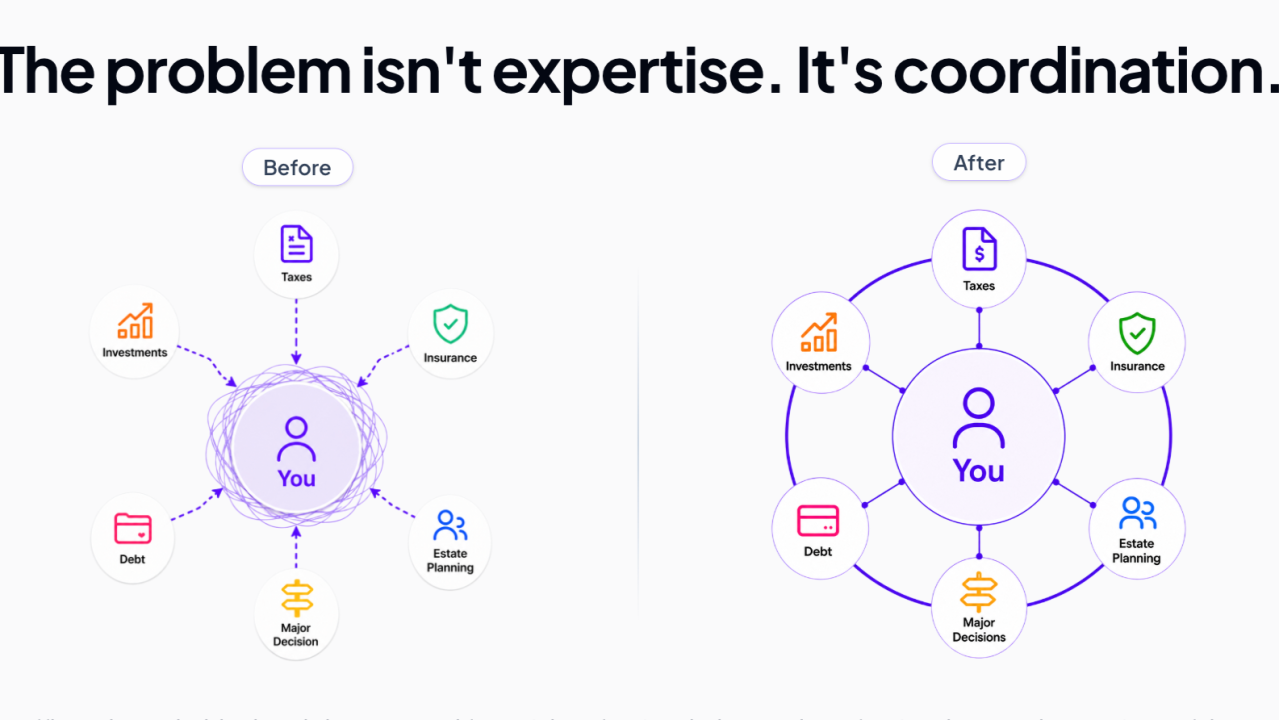

Affluent households often have excellent professionals but no coordination layer connecting taxes, investments, insurance, debt, equity compensation, and estate planning.

Consider a household with two high earners, equity compensation, a mortgage, brokerage and retirement accounts, life insurance, and an estate plan. They have a capable CPA, financial advisor, insurance broker, and attorney. Each professional may do excellent work, yet the household can still lose money when no one sees how every decision fits together.

That is the coordination gap. It is not a lack of expertise. It is the space between experts.

The problem was never expertise

A good CPA understands tax. A good advisor understands portfolio construction. A good attorney understands trusts and estate documents. The problem appears when a decision in one domain changes the outcome in another.

An investment decision can create a tax consequence that the CPA never had a chance to evaluate. Equity compensation can increase concentration outside the accounts an advisor manages. Cash, debt, retirement contributions, and a future vesting event may require several professional perspectives at the same time. Beneficiary designations can drift away from an estate plan when the documents are never compared.

Each professional can execute their assignment correctly while the household loses money through the handoffs.

Why the gap is structural

Affluent households usually engage professionals by specialty. The CPA is responsible for tax, the advisor for investments, the attorney for estate planning, and the broker for insurance. Their scope, compensation, and liability are built around those individual domains.

Coordination may happen occasionally, often around a specific document or deadline. What is usually missing is a standing process that asks whether an upcoming decision creates consequences elsewhere in the household's financial life.

The information is fragmented too. Tax returns, investment accounts, insurance policies, estate documents, equity compensation, and debt records live in different systems. Building the complete picture becomes a project, and keeping it current becomes a role that no one owns.

What the coordination gap costs

The cost is rarely one dramatic mistake. More often, it appears as a series of missed or poorly sequenced decisions:

- Investment gains realized without full tax context

- Concentration risk growing outside the advisor's managed accounts

- Cash, debt, and retirement decisions evaluated separately

- Tax-planning windows noticed after they close

- Insurance coverage drifting away from current household needs

- Estate documents and account designations falling out of alignment

One isolated decision may not look significant. Repeated across years of vesting events, rebalances, refinances, conversions, and family changes, the accumulated cost can become material.

Closing the gap does not replace the experts

The answer is not asking every specialist to become a generalist. The CPA should continue to own tax decisions. The advisor should continue to own portfolio decisions. The attorney should continue to own legal work.

What is missing is a coordination layer that maintains a current view of the household, identifies decisions that cross professional boundaries, and brings the right expert into the conversation at the right time.

With that layer in place, each professional keeps their authority and gains better context. The household gets continuity instead of rebuilding its financial picture for every decision.

The takeaway

Many of the most expensive mistakes in an affluent household happen between professional domains. No individual expert may be responsible for the gap, but the household still bears its cost.

Closing that gap requires one connected financial view and a process that keeps taxes, investments, insurance, debt, equity compensation, and estate planning aligned over time.

See your financial picture in one place

Book a free demo to see how Alpheva coordinates investments, taxes, insurance, estate planning, and the decisions between them.

Book your free demo